A credit score and a credit report are related but different parts of your financial profile. Read on to learn the difference.

Credit Report

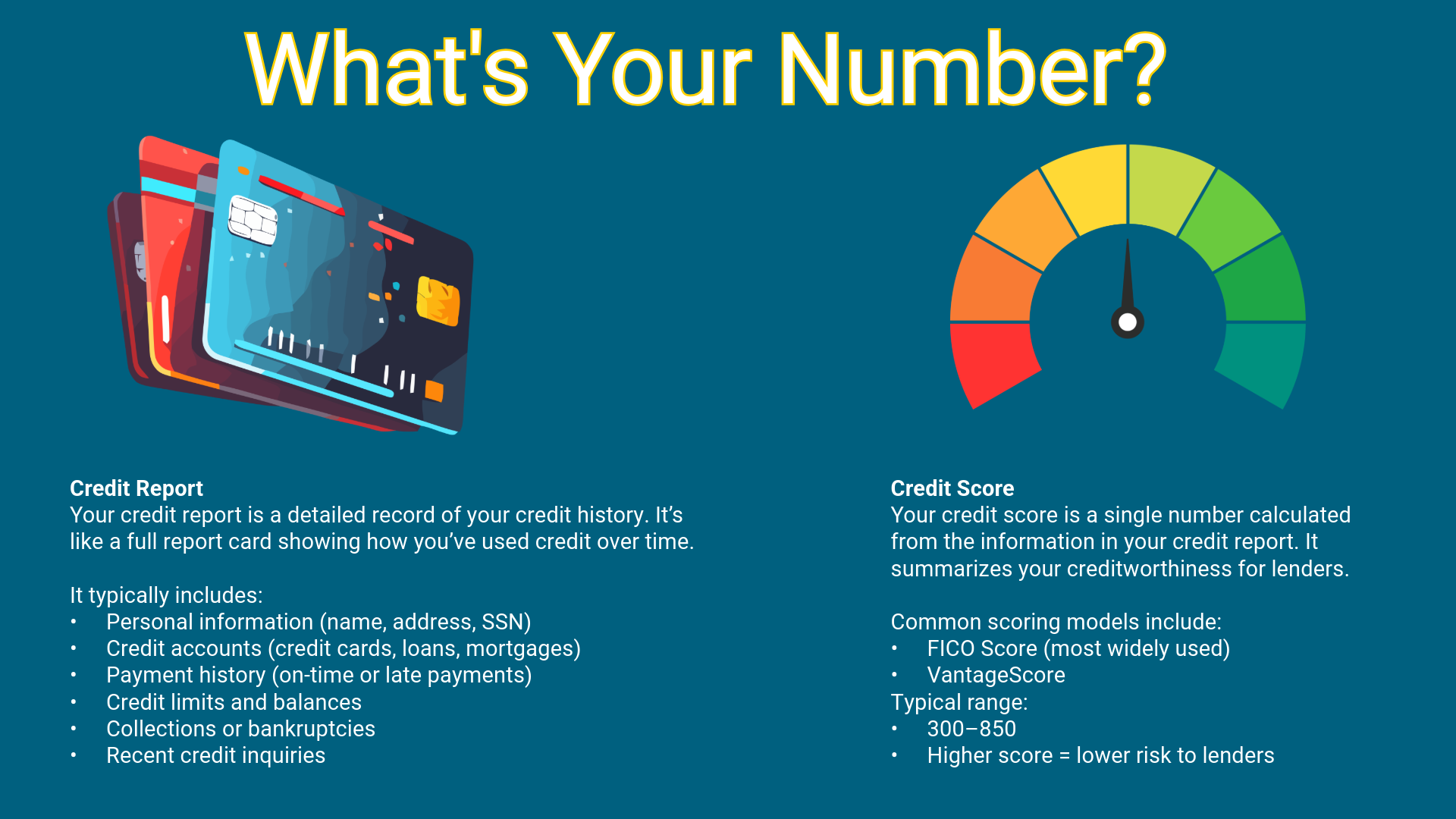

Your credit report is a detailed record of your credit history. It’s like a full report card showing how you’ve used credit over time.

It typically includes:

- Personal information (name, address, SSN)

- Credit accounts (credit cards, loans, mortgages)

- Payment history (on-time or late payments)

- Credit limits and balances

- Collections or bankruptcies

- Recent credit inquiries

In the U.S., the credit bureaus that compile these reports are:

- Equifax

- Experian

- TransUnion

You can check your reports for free through the official site run by the bureaus:

AnnualCreditReport.com.

Credit Score

Your credit score is a single number calculated from the information in your credit report. It summarizes your creditworthiness for lenders.

Common scoring models include:

- FICO Score (most widely used)

- VantageScore

Typical range:

- 300–850

- Higher score = lower risk to lenders

Factors affecting your score:

- Payment history

- Amount of debt

- Length of credit history

- Credit mix

- New credit inquiries

Simple Way to Think About It

- Credit report = the full history and details

- Credit score = the summary number based on that history

Example: A lender might pull your credit report from Experian and then look at your FICO Score to quickly judge your credit risk.

Tip: It’s incredibly important to check your credit report at least once a year to make sure there are no errors that could lower your score.