Building flexibility into a financial plan is less about predicting every future event and more about designing systems that can absorb change without derailing your goals. A resilient plan usually combines liquidity, adaptable spending, diversified income/assets, and regular reviews.

Here are the most effective ways to make your financial plans flexible:

Separate “Core Stability” from “Optional Growth”

Think of your finances in layers:

- Core layer: housing, insurance, emergency savings, retirement basics

- Flexible layer: travel, luxury purchases, aggressive investing, side projects

This structure lets you reduce discretionary spending during life changes without jeopardizing essentials.

Maintain a Strong Emergency Fund

A flexible plan needs cash reserves.

Typical targets:

- 3–6 months of expenses for stable dual-income households

- 6–12 months if self-employed, single-income, or in a volatile industry

Keep it somewhere liquid and safe, such as a high-yield savings account.

This protects against:

- Job loss

- Medical issues

- Relocation

- Family changes

- Unexpected repairs

Avoid Overcommitting to Fixed Expenses

High fixed costs reduce adaptability.

Watch for:

- Oversized mortgages or rent

- Large car payments

- Excessive subscriptions

- Debt-heavy lifestyles

A useful benchmark:

- Keep mandatory monthly obligations low enough that your plan still works if income temporarily drops.

Build Multiple Income Streams

Flexibility increases when all income doesn’t depend on one source.

Examples:

- Side consulting

- Freelance work

- Rental income

- Dividend investments

- Small online businesses

- Professional certifications that improve employability

Even modest secondary income can create breathing room during transitions.

Diversify Investments by Time Horizon

Match money to when you may need it.

Example structure:

- Short-term (0–3 years): cash, treasury funds

- Medium-term (3–10 years): balanced investments

- Long-term (10+ years): growth-oriented assets

This reduces the chance you’ll need to sell long-term investments during a downturn because of a life event.

Use Scenario Planning

Instead of making one “perfect” plan, prepare for several realistic possibilities.

Ask:

- What if my income drops 20%?

- What if I move cities?

- What if I have children?

- What if I want a career break?

- What if I need to support parents?

You don’t need exact answers — just rough contingency plans.

Review Insurance Regularly

Insurance is what keeps one life event from becoming a financial crisis.

Key areas:

- Health insurance

- Disability insurance

- Life insurance (if others depend on you)

- Home/renters insurance

- Umbrella liability coverage for higher net worth households

Update coverage after major life changes.

Keep Debt Strategic, Not Burdensome

Not all debt is bad, but inflexible debt is risky.

Prioritize:

- Reasonable debt-to-income ratios

- Fixed-rate borrowing when appropriate

- Accelerated payoff of high-interest debt

Avoid relying on future income growth to make current obligations manageable.

Revisit Your Plan Regularly

A flexible plan is a living system.

Review:

- Quarterly for budgeting/cash flow

- Annually for investments and goals

- Immediately after major life events

Common triggers:

- Marriage/divorce

- New child

- Career change

- Move

- Inheritance

- Health changes

Focus on Financial Capacity, Not Just Net Worth

Many people optimize for maximum returns but ignore resilience.

Useful metrics include:

- Savings rate

- Liquidity

- Low fixed expenses

- Employable skills

- Geographic flexibility

- Stress-tested budget

A slightly less optimized plan that survives disruption is often better than an aggressive plan that breaks under pressure.

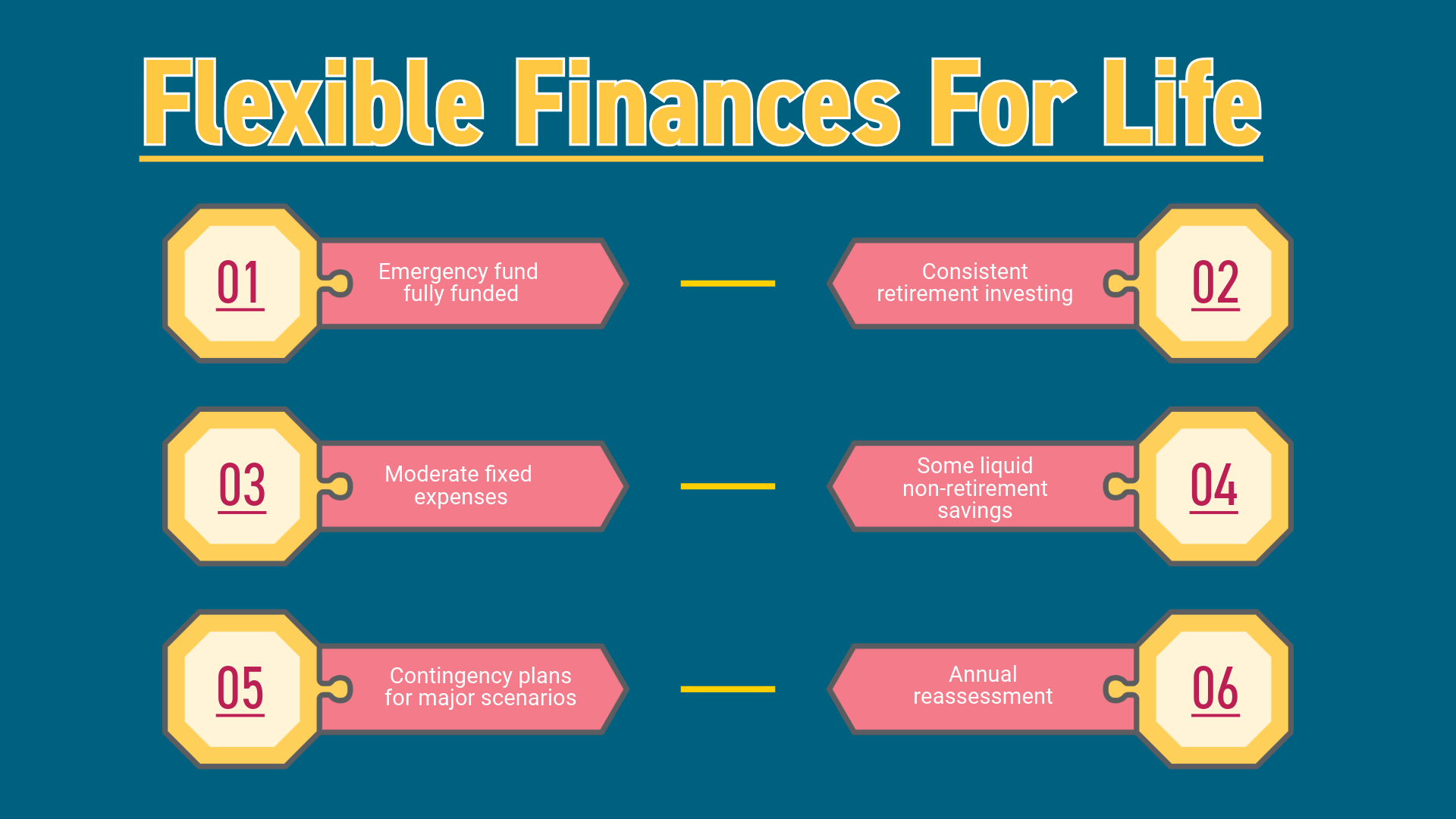

A Practical Framework

A flexible financial plan often looks like:

- Emergency fund fully funded

- Moderate fixed expenses

- Consistent retirement investing

- Some liquid non-retirement savings

- Insurance coverage updated

- Contingency plans for major scenarios

- Annual reassessment

That combination gives you room to adapt when life changes without starting over financially.