An FSA (Flexible Spending Account) and an HSA (Health Savings Account) are both tax-advantaged accounts used to pay for healthcare expenses—but they differ in some important ways.

Those differences include:

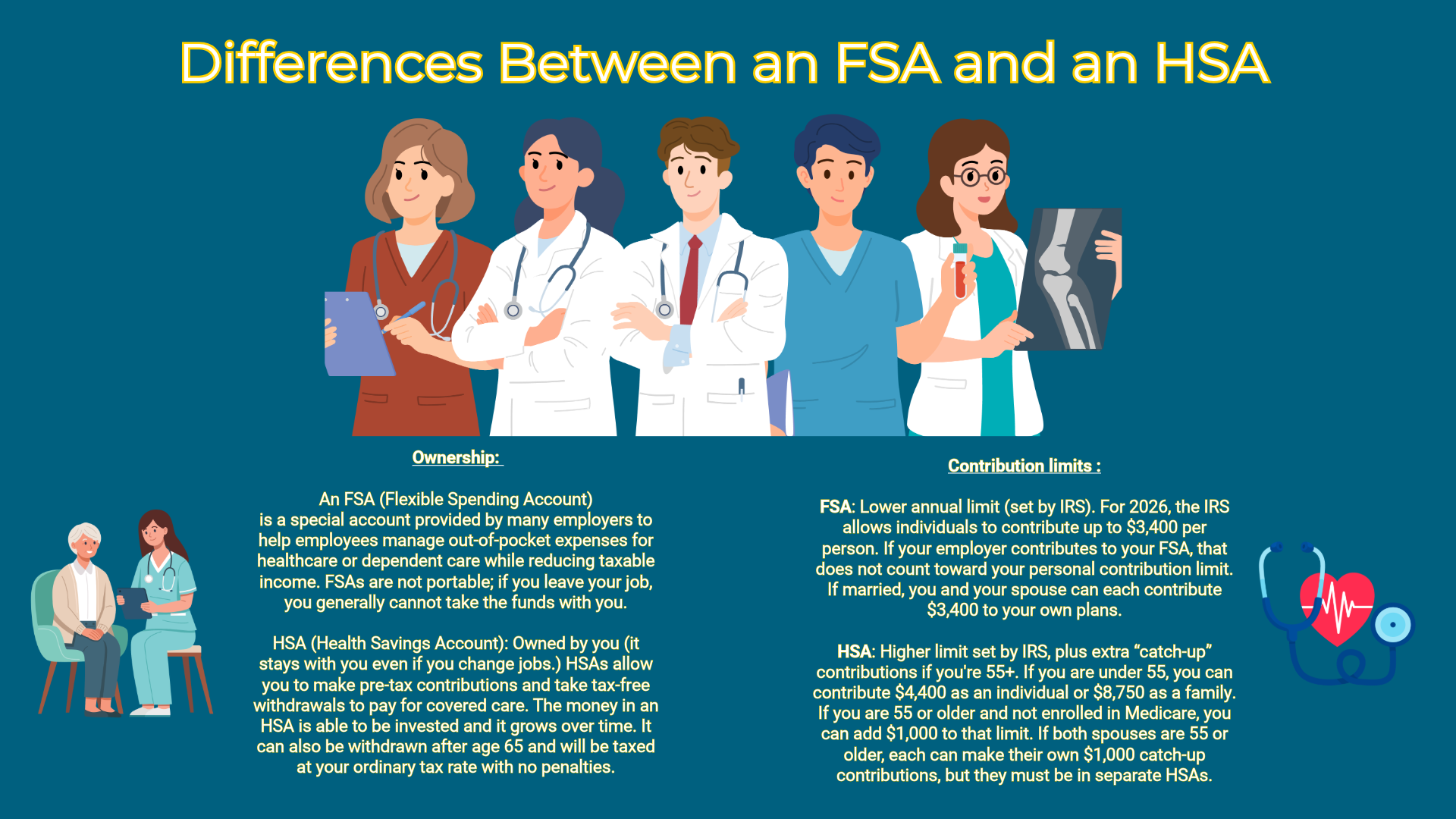

Ownership

FSA: Owned by your employer, FSAs are special accounts that are provided by many employers to help employees manage out-of-pocket expenses for healthcare or dependent care while reducing taxable income. FSAs are not portable; if you leave your job, you generally cannot take the funds with you.

HSA: Owned by you (it stays with you even if you change jobs.) HSAs allow you to make pre-tax contributions and take tax-free withdrawals to pay for covered care. The money in an HSA is able to be invested and it grows over time. It can also be withdrawn after age 65 and will be taxed at your ordinary tax rate with no penalties.

Eligibility

- FSA: Available with most employer health plans.

- HSA: Only available if you have a high-deductible health plan (HDHP). This is defined as a plan with a minimum deductible of $1,700 for an individual or $3,400 as a family, with a maximum out-of-pocket limit for $8,500 for individuals or $17,000 for families.

Contribution limits

- FSA: Lower annual limit (set by IRS). For 2026, the IRS allows individuals to contribute up to $3,400 per person. If your employer contributes to your FSA, that does not count toward your personal contribution limit. If married, you and your spouse can each contribute $3,400 to your own plans.

- HSA: Higher limit set by IRS, plus extra “catch-up” contributions if you're 55+. If you are under 55, you can contribute $4,400 as an individual or $8,750 as a family. If you are 55 or older and not enrolled in Medicare, you can add $1,000 to that limit. If both spouses are 55 or older, each can make their own $1,000 catch-up contributions, but they must be in separate HSAs.

Rollover rules

- FSA: Use it or lose it (some plans allow a small rollover or grace period; ask your employer).

- HSA: Funds roll over indefinitely—no expiration date.

Investment options

- FSA: No investing—just spend the money.

- HSA: Can be invested (like a retirement account) once balance reaches a threshold.

Tax advantages

Both offer tax benefits, but HSAs have a triple tax advantage:

- Contributions are tax-deductible

- Growth is tax-free

- Withdrawals for qualified medical expenses are tax-free

FSAs offer:

- Pre-tax contributions

- Tax-free withdrawals for medical expenses

Portability

- FSA: Usually lost if you leave your job

- HSA: Goes with you forever

Simple way to think about it:

- FSA = short-term spending tool (good for predictable yearly expenses)

- HSA = long-term savings + investing tool (can double as a retirement account)