A useful way to think about financial milestones is by decade: each stage shifts from building stability to increasing optionality to preserving freedom. The exact numbers depend on income, family situation, and cost of living, but these are strong benchmarks to aim toward.

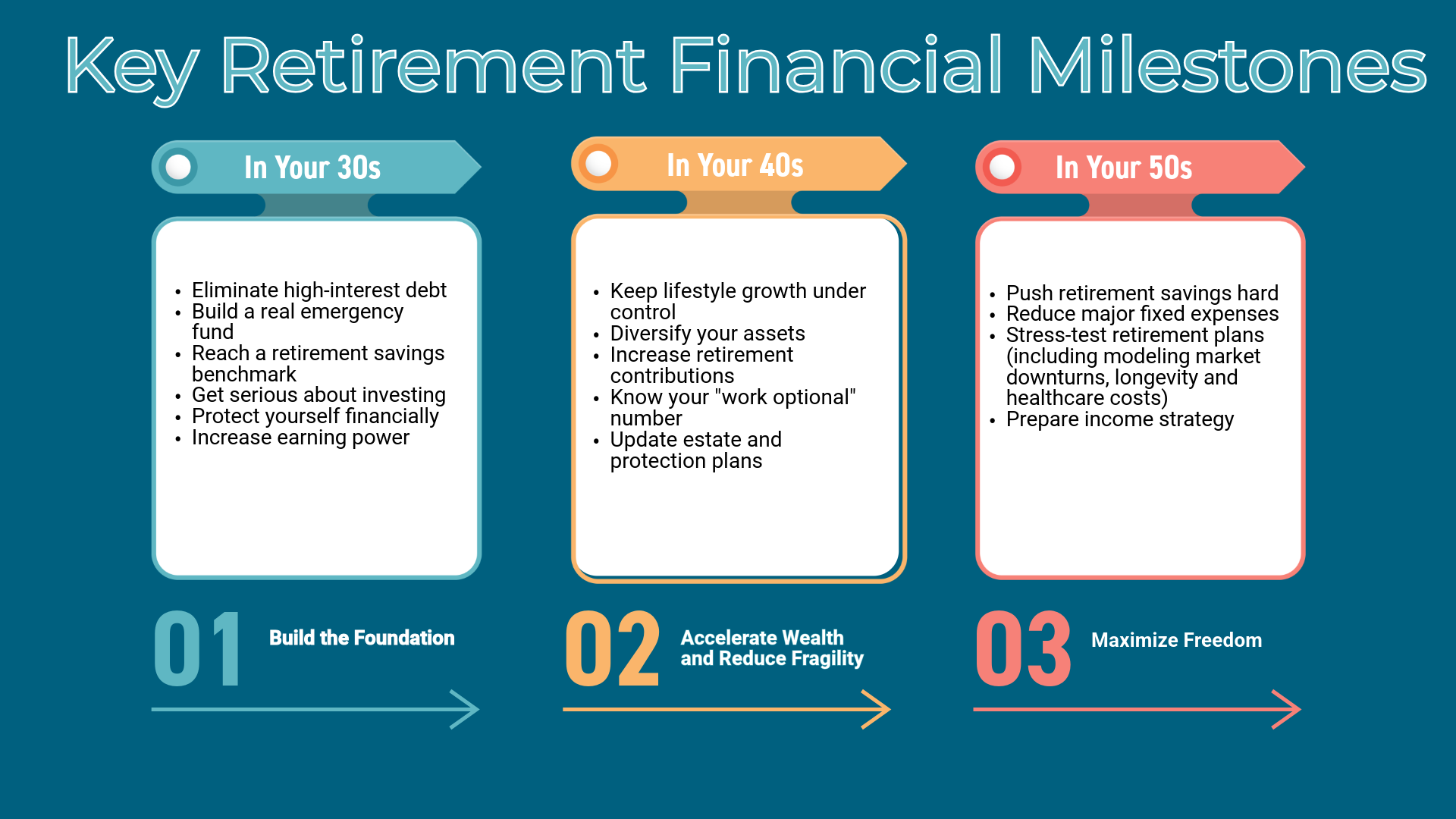

Your 30s: Build the Foundation

Eliminate high-interest debt

Priority debts:

- Credit cards

- Payday/personal loans

- High-rate private student loans

A mortgage or low-rate federal student loans are usually less urgent.

Build a real emergency fund

Target:

- 3–6 months of essential expenses

- Closer to 6–12 months if self-employed, single-income household, or volatile industry

Keep this in a high-yield savings account.

Reach a retirement savings benchmark

A common target:

- 1× your annual salary saved for retirement by age 30

- 2× by age 35

This includes:

- 401(k)

- IRA

- Roth IRA

- Pension balances

Get serious about investing

Aim to invest:

- 15–25% of gross income over time

Key habits matter more than stock-picking:

- Automate contributions

- Use diversified low-cost index funds

- Avoid lifestyle inflation

Protect yourself financially

Important protections:

- Health insurance

- Disability insurance

- Term life insurance if others depend on your income

- Basic estate documents (will, beneficiaries, healthcare directives)

Increase earning power

Your 30s are often the highest-ROI decade for:

- Skill development

- Career pivots

- Negotiating compensation

- Building side income or ownership stakes

Income growth early dramatically compounds later.

Your 40s: Accelerate Wealth and Reduce Fragility

Retirement savings targets

Typical benchmarks:

- 3× salary by 40

- 6× salary by 50

If behind, this is the decade to aggressively catch up.

Keep lifestyle growth under control

Many people hit peak spending in their 40s:

- Larger homes

- Kids’ expenses

- Cars

- Travel

- Tuition

Try to direct raises toward:

- Investments

- Mortgage reduction

- Tax-advantaged accounts

Diversify your assets

You ideally want wealth beyond just:

- Your primary home

- Your employer stock

- Your paycheck

Possible additions:

- Taxable brokerage account

- Real estate

- Small business equity

- HSAs

- 529 plans if you have children

Increase retirement contributions

Take full advantage of:

- Employer match

- IRA limits

- HSA investing

- Catch-up contributions later in the decade

Know your “work optional” number (i.e., when you can retire.)

Estimate:

- Annual spending

- Desired retirement age

- Safe withdrawal assumptions

Many people in their 40s realize the goal is not “never work again,” but having leverage and flexibility.

Update estate and protection plans

Especially important if you have:

- Children

- Property

- Aging parents

- Business interests

Review:

- Will/trust

- Guardianship plans

- Insurance coverage

- Beneficiaries

Your 50s: Maximize Freedom

Push retirement savings hard

This is often peak earning years.

Targets:

- 8× salary by 60

- Higher if retiring early

Use catch-up contributions aggressively.

Reduce major fixed expenses

Try entering retirement with:

- Lower housing costs

- Minimal consumer debt

- Predictable healthcare planning

Stress-test retirement plans

Model:

- Market downturns

- Longevity

- Healthcare costs

- Long-term care needs

- Supporting family members

Prepare income strategy

Think beyond “portfolio size”:

- Social Security timing

- Tax-efficient withdrawals

- Roth conversions

- Pension options

- Required minimum distributions

Your 60s and Beyond: Preserve Independence

Transition from accumulation to sustainability

The focus shifts toward:

- Reliable income

- Tax efficiency

- Risk management

- Estate planning

Manage withdrawal rates carefully

A common starting framework:

- Around 3–4% annual withdrawals from investments

- Adjust based on market conditions and flexibility

Plan for healthcare and long-term care

Healthcare becomes one of the largest retirement expenses.

Understand:

- Medicare

- Supplemental coverage

- Long-term care options

- Estate implications

Simplify finances

As complexity grows, simplification becomes valuable:

- Consolidate accounts

- Organize documents

- Reduce unnecessary risk

- Ensure trusted family members/executors can navigate your finances

Milestones That Matter at Any Age

Regardless of decade, strong financial health usually means:

- Spending less than you earn

- Avoiding destructive debt

- Investing consistently

- Increasing income over time

- Maintaining flexibility

- Protecting against catastrophe

- Aligning money with your actual priorities

A Simple “Healthy Progress” Snapshot

By your:

- 30s: stable, invested, protected

- 40s: accumulating serious assets

- 50s: financially flexible

- 60s+: financially independent and resilient

You do not need perfect timing or perfect decisions. Consistency over decades matters far more than optimization.