You can’t guarantee with absolute certainty that you’ll never outlive your retirement savings—but you can make it unlikely with a solid, layered strategy. The key is balancing withdrawals, investment growth, and risk protection.

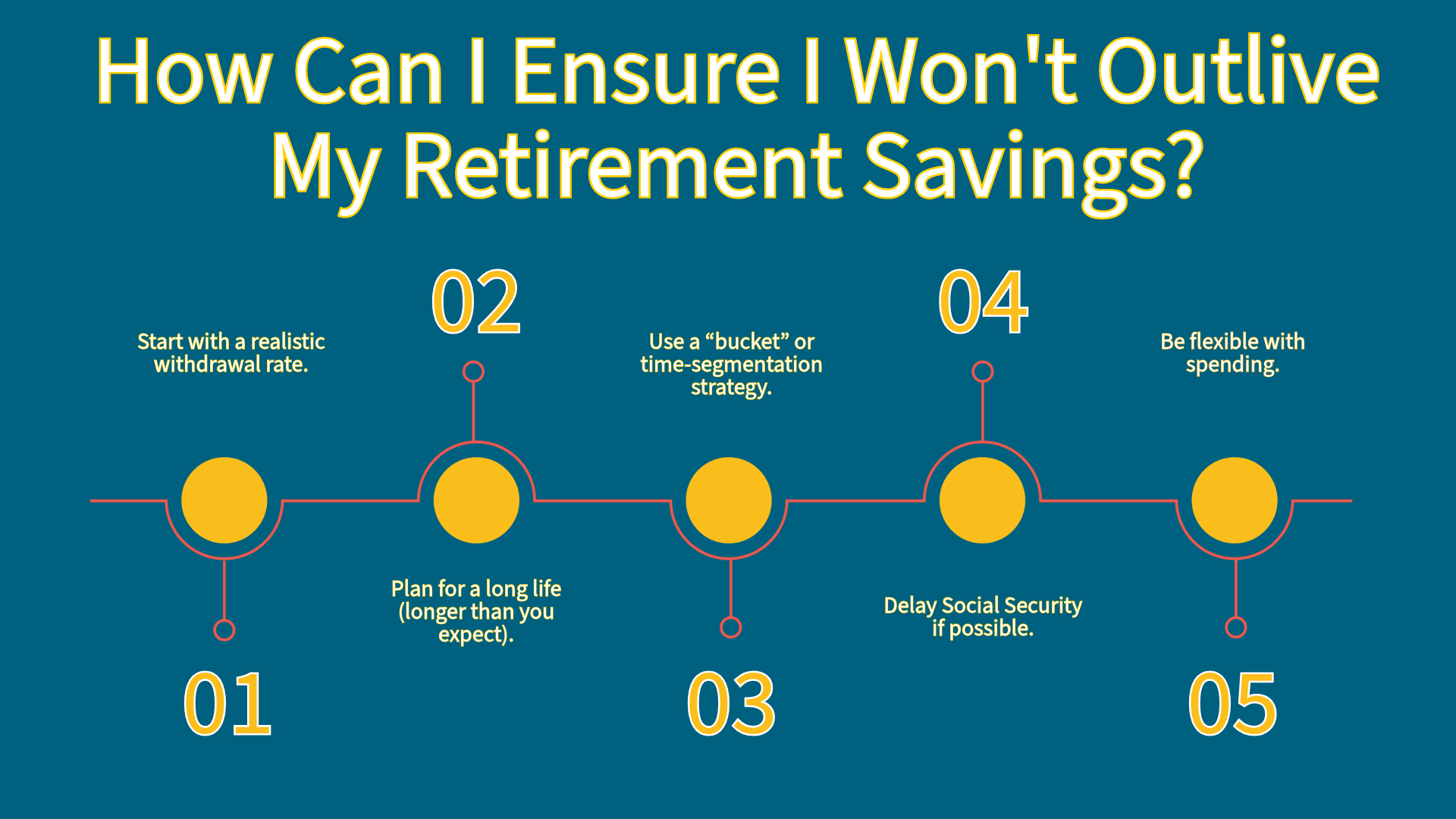

Start with a realistic withdrawal rate

A common guideline is the 4% rule, based on retirement finance research. It suggests withdrawing less than 4% of your portfolio in year one, then adjusting for inflation annually.

- Conservative planners today often suggest 3–3.5% to be safer, especially with longer lifespans and market uncertainty.

Plan for a long life (longer than you expect)

Longevity risk is one of the biggest variables. It’s wise to plan to at least age 90–95. This aligns with findings from groups like Society of Actuaries, which highlight increasing life expectancy.

Use a “bucket” or time-segmentation strategy

Divide your money into:

- Short-term (0–3 years): cash or very safe assets

- Mid-term (3–10 years): bonds or conservative investments

- Long-term (10+ years): stocks for growth

This helps you avoid selling investments during market downturns.

Stay invested for growth

Inflation quietly erodes purchasing power. Exposure to equities helps your portfolio grow over time. Many retirees stay 40–60% in stocks depending on risk tolerance.

Be flexible with spending

Rigid withdrawals can be dangerous. Instead:

- Spend a bit less after bad market years

- Allow modest increases after strong years

This dynamic approach significantly improves success rates.

Delay Social Security if possible

Delaying benefits (up to age 70 in the U.S.) increases guaranteed lifetime income. This reduces pressure on your portfolio later.

Consider guaranteed income sources

Products like annuities can provide a “floor” of income. For example, offerings from companies like Vanguard or Fidelity Investments sometimes include annuity options.

They’re not always ideal, but they can hedge longevity risk.

Manage healthcare and long-term care risk

Healthcare costs are a major wildcard. Planning for long-term care—either via savings or insurance—prevents unexpected depletion.

Rebalance and review annually

Your plan isn’t “set and forget.” Revisit:

- Withdrawal rate

- Market performance

- Spending needs

Adjust as conditions change.

The big picture

Think of retirement security as a combination of:

- Sustainable withdrawals

- Growth investments

- Guaranteed income

- Flexibility

- You don’t have to do this alone. Consult with a registered financial adviser.