Paying only the minimum on a credit card does technically reduce your balance—but so slowly that it can feel like it’s not going down at all. The main reason is interest and how payments are applied.

Here’s what’s happening behind the scenes:

Most of your payment goes to interest first.

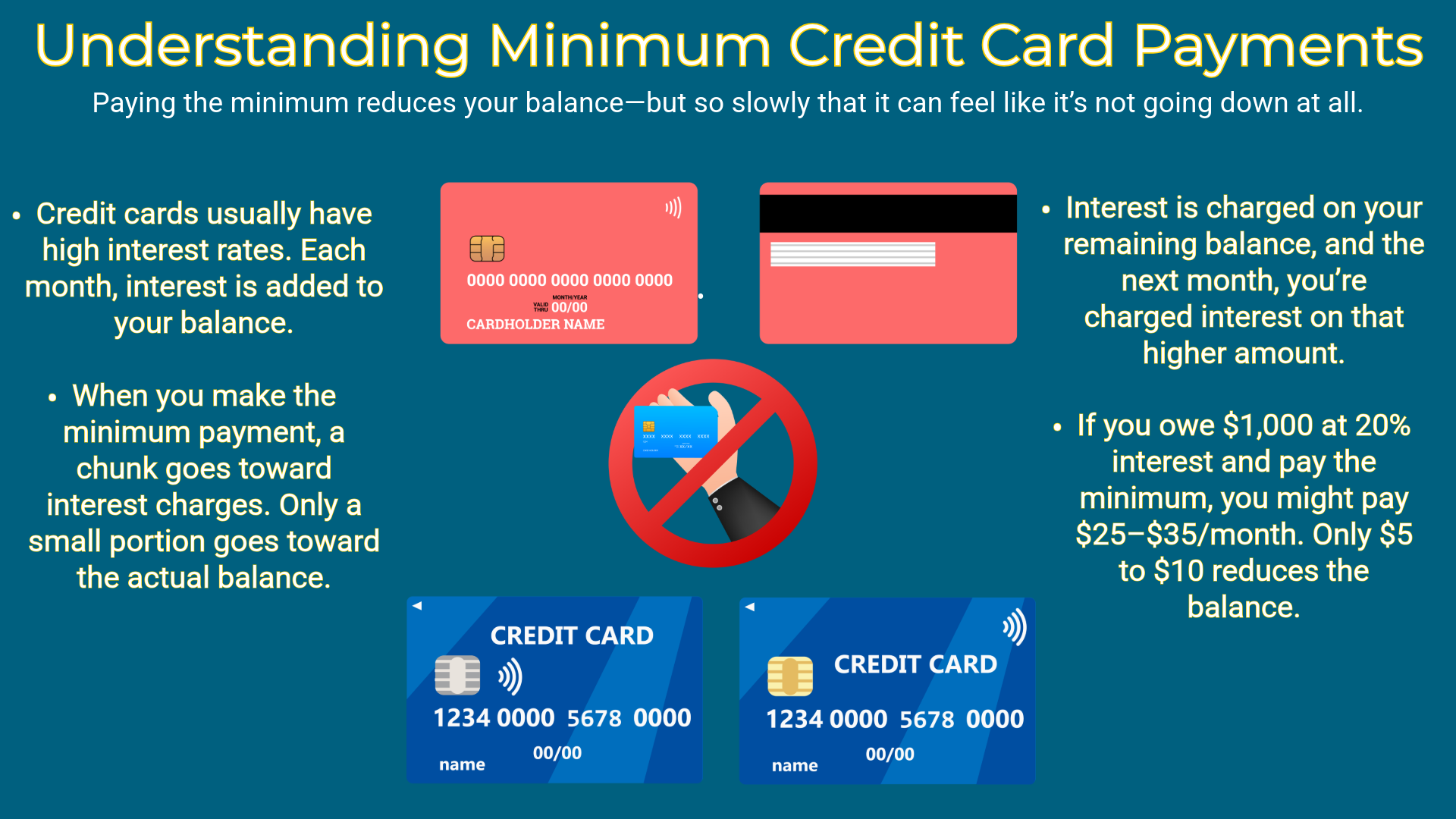

Credit cards usually have high interest rates (often 15–30% APR). Each month, interest is added to your balance. When you make the minimum payment:

- A chunk goes toward interest charges.

- Only a small portion goes toward the actual balance (principal).

So, your debt barely shrinks.

New purchases can cancel out progress

If you keep using the card:

- New charges and interest can equal or exceed your payment.

- This can make your balance stay the same—or even grow.

Minimum payments are designed to be small.

Credit card companies often set the minimum as:

- A percentage of your balance (e.g., 1–3%)

- Or a flat amount (like $25–$40)

That amount is intentionally low, which:

- Keeps your account in good standing but stretches repayment over many years.

Compounding interest works against you.

Interest is charged on your remaining balance, and then:

- Next month, you’re charged interest on that new higher amount.

- This is called compound interest, and it slows payoff dramatically.

Simple example

If you owe $1,000 at 20% interest and only pay the minimum:

- You might pay $25–$35/month.

- Only $5–$10 reduces the balance.

- The rest covers interest.

It can take years to pay off—and cost hundreds extra.

Bottom line: Paying the minimum keeps you from missing payments but barely reduces your debt. Whenever possible, pay more than the minimum amount.