Avoiding a few common money mistakes can make a big difference over time. Here are some of the biggest ones—and what to do instead:

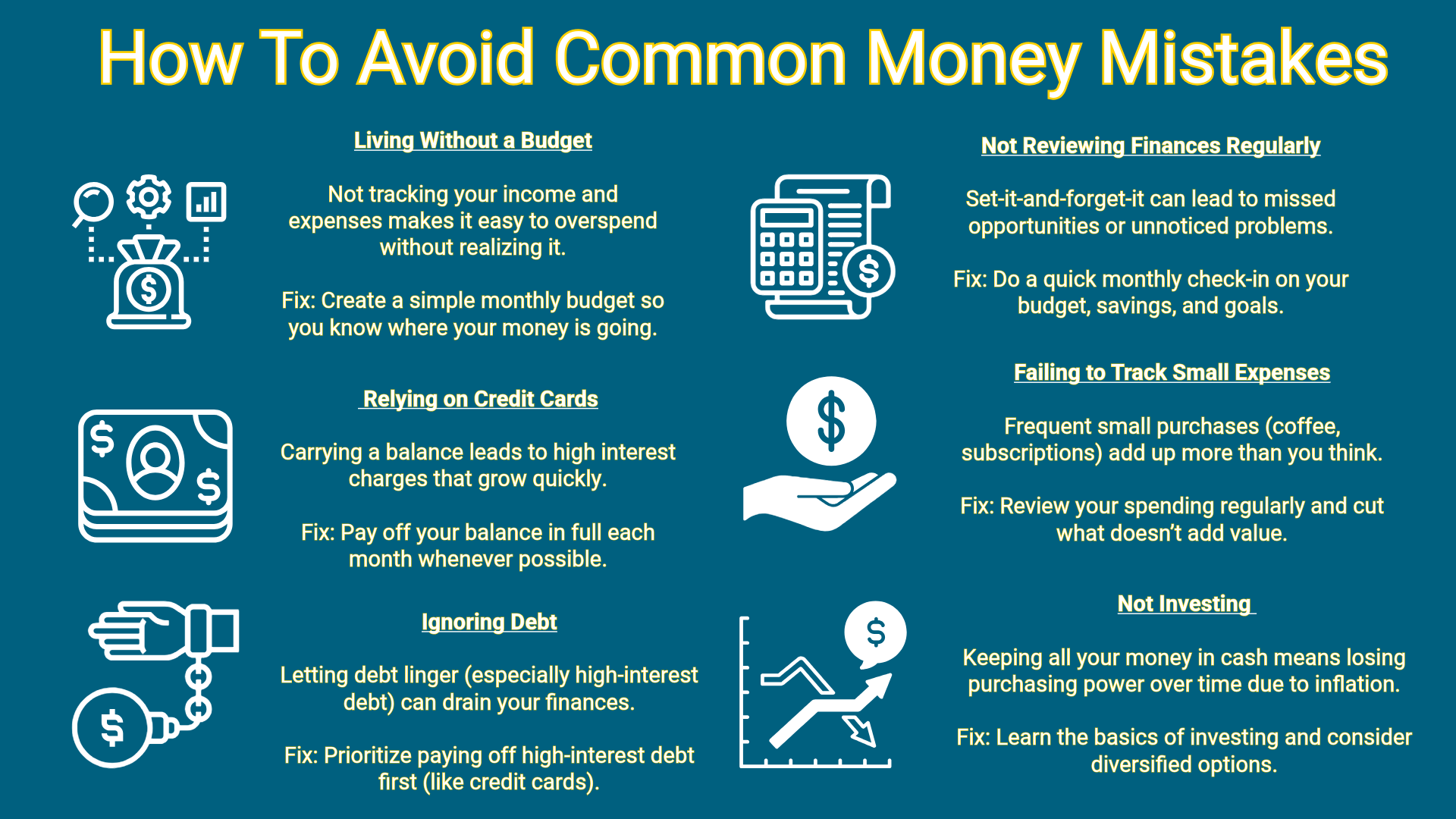

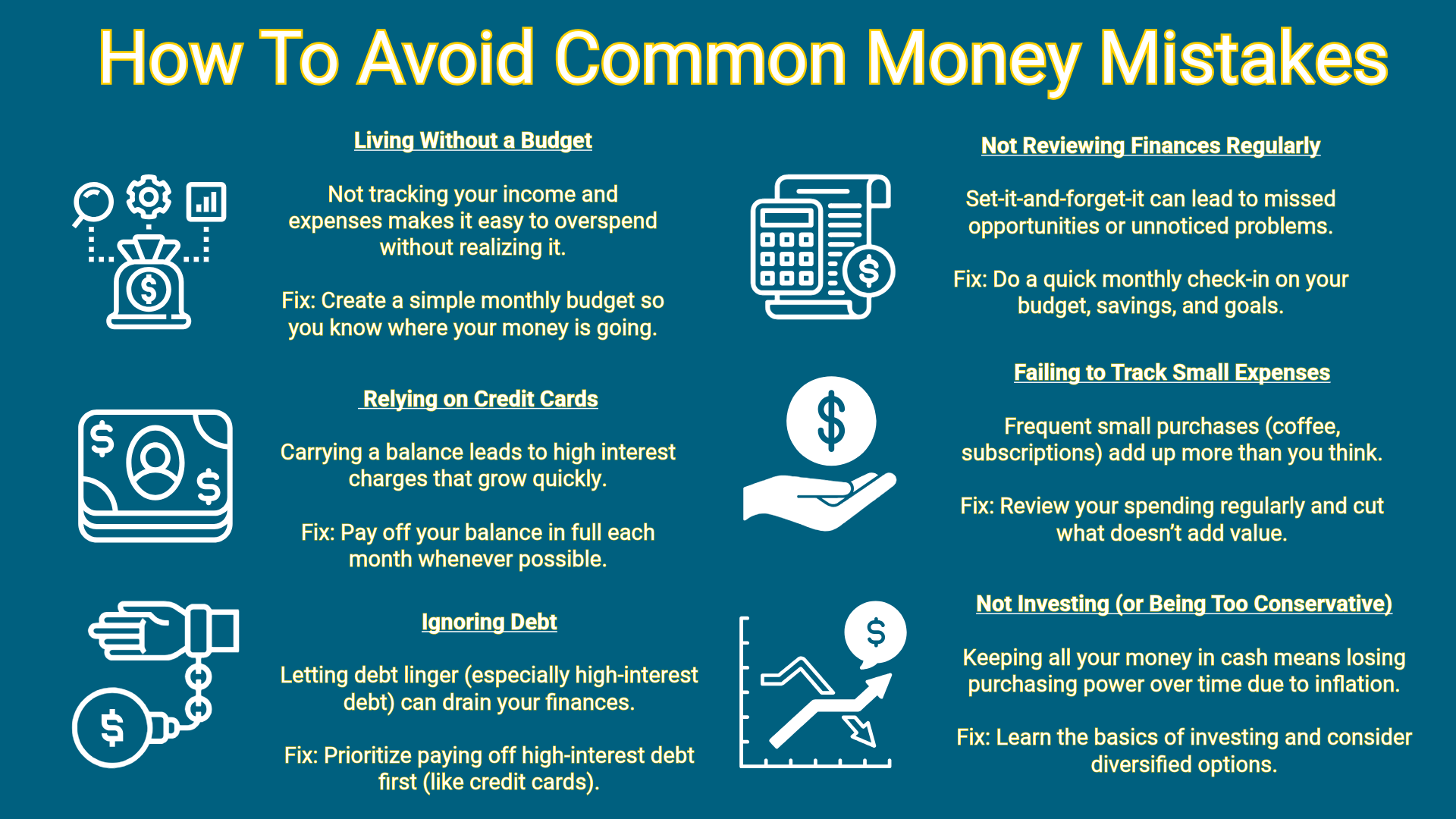

Living Without a Budget

Not tracking your income and expenses makes it easy to overspend without realizing it.

Fix: Create a simple monthly budget so you know where your money is going.

Ignoring an Emergency Fund

Unexpected expenses (car repairs, medical bills) can push you into debt if you’re unprepared.

Fix: Aim to save 3–6 months of essential expenses in a separate account.

Relying Too Much on Credit Cards

Carrying a balance leads to high interest charges that grow quickly.

Fix: Pay off your balance in full each month whenever possible.

Not Saving for Retirement Early

Delaying retirement savings means missing out on compound growth (Compound Interest).

Fix: Start early—even small contributions add up over time.

Lifestyle Inflation

As income increases, spending often rises just as fast.

Fix: Keep your expenses in check and increase savings when you earn more.

Not Setting Financial Goals

Without clear goals, it’s easy to drift and make impulsive decisions.

Fix: Set short-term (vacation, emergency fund) and long-term goals (home, retirement).

Ignoring Debt

Letting debt linger (especially high-interest debt) drain your finances.

Fix: Prioritize paying off high-interest debt first (like credit cards).

Not Investing

Keeping all your money in cash means losing purchasing power over time due to inflation.

Fix: Learn the basics of investing and consider diversified options.

Failing to Track Small Expenses

Frequent small purchases (coffee, subscriptions) add up more than you think.

Fix: Review your spending regularly and cut what doesn’t add value.

Not Reviewing Finances Regularly

Set-it-and-forget-it can lead to missed opportunities or unnoticed problems.

Fix: Do a quick monthly check-in on your budget, savings, and goals.