Refinancing your home can save you thousands, but the timing matters. Here are the key situations when it makes sense to consider refinancing:

When Interest Rates Have Dropped

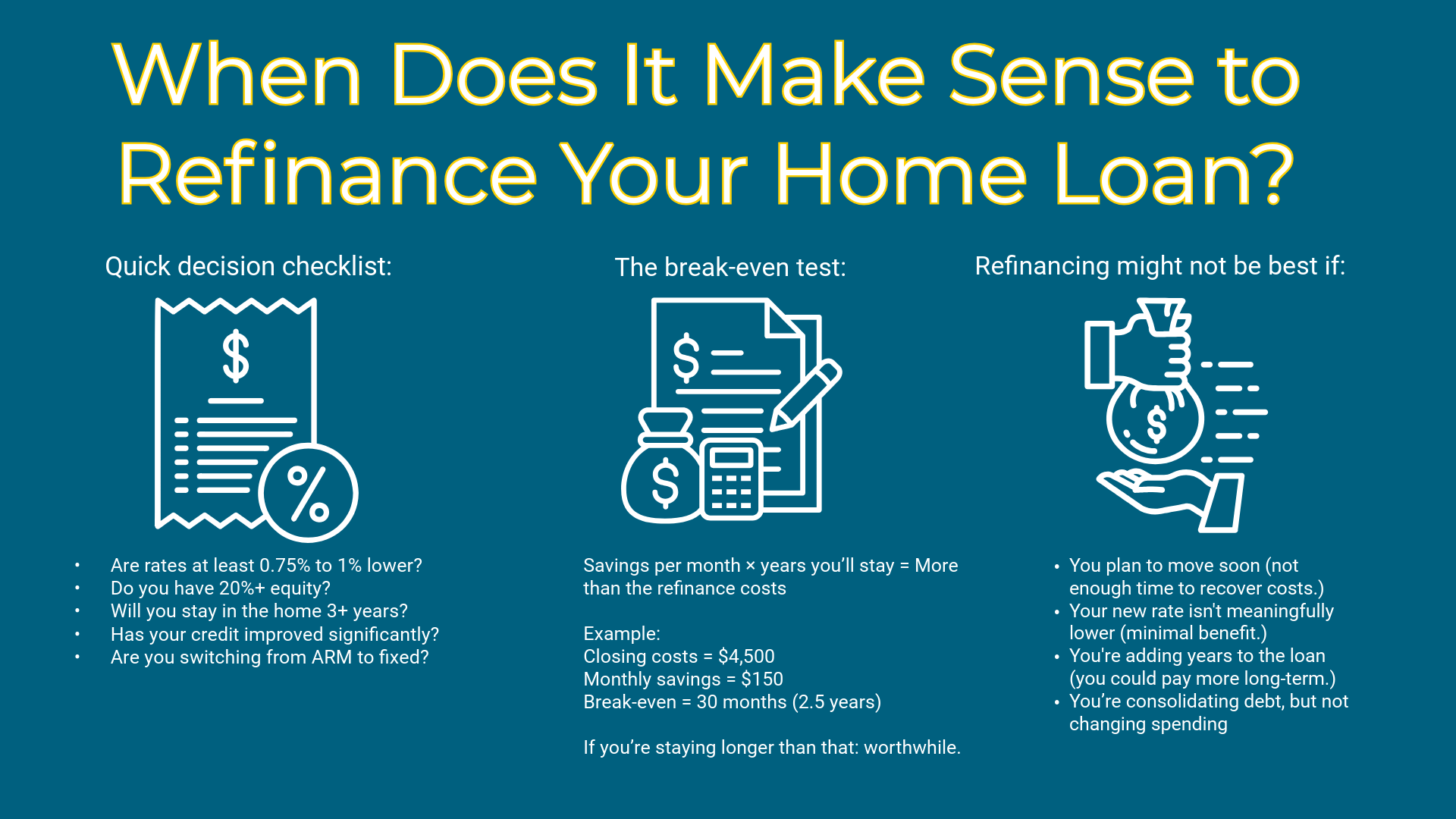

A common rule of thumb:

Refinance if rates are at least 0.75%–1% lower than your current rate

Why?

- Lowers your monthly payment

- Reduces total interest paid over the life of the loan

Best for homeowners planning to stay long enough to recoup closing costs (often 2–5 years).

When You Want to Shorten Your Loan Term

Moving from:

- 30-year to 15-year

- Or 20-year to 10-year

Benefits:

- Pay off the home faster

- Pay far less in total interest

- Build equity more quickly

Payments are usually higher, but long-term savings can be significant.

When You Want to Switch from an Adjustable-Rate Mortgage

Consider refinancing if you have an ARM (Adjustable-Rate Mortgage) and:

- Your rate is about to reset

- You are uncomfortable with rate unpredictability

Switching to a fixed rate adds payment stability and removes risk during rising-rate periods.

To Access Equity (Cash-Out Refinance)

You can exercise this option if you will have at least 20% equity remaining after the transaction.

Useful for:

- Home renovations

- Debt consolidation

- Major expenses (college, medical, etc.)

Only beneficial if you won’t be tempted to use it like a credit card — remember, this increases your mortgage balance.

When Your Credit Score Has Improved

If your score has jumped significantly since your original loan (for example, 640 to 720):

- You may now qualify for a lower rate

- Better loan products

- Lower private mortgage insurance (PMI)

When You Can Remove Private Mortgage Insurance

If your equity has reached 20% or more, refinancing can eliminate PMI and lower your payment.

This happens from:

- Paying down principal

- Home value increasing

- Major renovations

The Break-Even Test

Refinancing usually has closing costs (2–5% of loan amount).

You should refinance if:

Savings per month × Years you’ll stay = More than the refinance costs

Example:

- Closing costs = $4,500

- Monthly savings = $150

- Break-even = 30 months (2.5 years)

If you’re staying longer than that: worthwhile.

When refinancing might not be best:

- You plan to move soon (not enough time to recover costs)

- Your new rate isn’t meaningfully lower (minimal benefit)

- You’re adding years to the loan (you could pay more long-term)

- You’re consolidating debt, but not changing spending

Pros of refinancing:

Lower monthly mortgage payment

If you secure a lower interest rate, your monthly payment can decrease — freeing up cash for other goals.

Reduce total interest paid

A lower rate or a shorter loan term (e.g., switching from 30-year to 15-year) can dramatically reduce the interest you pay over the life of the loan.

Switch from adjustable to fixed rate

- Moving from an ARM to a fixed-rate mortgage offers stability and protection from future rate increases.

Opportunity for cash-out

A cash-out refinance allows you to tap home equity for:

- Home improvements

- Debt consolidation

- Large expenses

Remove or reduce PMI

- If your equity is now above 20%, refinancing may eliminate Private Mortgage Insurance.

Consolidate higher-interest debt

- Credit card debt at 20% vs. mortgage rate in the single digits? Refinancing could lower interest costs.

(Only beneficial if spending habits are controlled.)

Cons of Refinancing

Closing Costs

Refinancing usually costs 2–5% of the loan amount in closing fees — thousands of dollars up front.

You Might Extend Your Debt Timeline

Restarting a 30-year mortgage—even at a lower payment—may mean paying more interest total over time.

Monthly Savings May Not Outweigh Costs

If you move or sell within a couple of years, you may not break even on the refinance expense.

Cash-Out Adds More Debt:

You’re borrowing against your home.

If spending or emergencies continue, you may end up with:

- Higher mortgage

- Lower equity

- More total debt

Qualification Requirements

If:

- Your credit score dropped

- Your debt increased

- Your income changed

You may not receive favorable rates or approval.

Risk of Resetting Amortization

Early mortgage years are interest heavy — restarting the clock means paying interest-heavy years again.